For AXA this year 2020 represents a new challenge. Since June 2019 we have enlarged our team by hiring Simona Busetti who is responsible for broker management in the Italian market. Since the beginning of the year, for the first time in Ticino, we also have a dedicated credit underwriter, Andrea Pugliatti, focused on the analysis of Italian risks and, in general, the Ticino market.

This move on our part will bring added value for our customers, who will now have a key reference point for the analysis of debtors directly in Lugano. With Andrea, we will be able to offer our clients even more personalized and high-value advice.

In terms of market environment; at a global level, after years of stability, we see a stagnant economy, with an expected growth of 2.5% of GDP compared to 2.4% in 2019 (source world bank). For Italy, growth expectations for 2020 were +0.2%, which currently seem unlikely given the impact of the coronavirus, which is leading Italy into a technical recession (government source).

The steel sector in Italy, but also in Europe, is being significantly impacted by:

– the US-China tariff war, strengthening the influx of Chinese products into the EU despite the clauses established by the EU Commission to prevent this,

– the strong increase in raw materials used in the sector, from iron ore to coke

– overcapacity for already high inventories

– ILVA affair, where ArcelorMittal has created, and is still creating, difficulties for the industrial sector , especially mechanics.

Steel production in Italy, after a good 2018, suffered a contraction in 2019 of -4.1%, driven by the crisis in the automotive sector and the static demand for rebar, against a global production growth of 3.9%. Demand remains compressed for coils and carbon steel sheets, mainly due to low import prices from Turkey. The latter is contributing on several fronts such as the drop in nickel prices since the end of 2019.

In Europe, insolvencies, after a stagnant period, increased again by 2% on average, with some countries improving and some stable countries such as Italy. One of the key factors for the slow recovery of the Italian economy is certainly linked to political uncertainty and the lack of reforms.

This excludes the potential impact of Coronavirus on the health of Italian and other European companies with supply and order problems, which will emerge in the next months/years.

AXA’s commitment in trade credit insurance remains strong and will continue to develop its offering and risk analysis services in its current key markets; Switzerland, Italy, Germany, Spain, Morocco and Singapore.

https://www.lcta.ch/site/wp-content/uploads/2020/06/ART-Axa-Ticino-wolfgang-hasselmann-7CPepk1NCns-unsplash.jpg10671600lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-06-26 12:00:002020-06-26 12:00:00AXA expands its team in Ticino

This year the Lugano Commodity Trading Association (LCTA) celebrates its 10th anniversary. LCTA is a non-profit organization that brings together operators active in the commodity trading, shipping, insurance and financing of this sector. In order to comment on the growth and evolution of the association, we interviewed the president, Thomas Patrick.

What has LCTA done for the commodity trading industry over the years?

LCTA originally formed in 2010 as an association of 8 members all active in the commodity sector with an initial primary goal to improve the understanding of the economic contribution made by the commodity trading in Ticino. Commodity trading does not have brand name recognition and as such does not depend on advertising as a marketing medium to sale products; which makes the sector uniquely private. Commodities companies are rarely listed (Glencore being an exception) with the majority privately owned and often including management as shareholders. Other stakeholders include the banks, insurance companies, ship brokers, warehousing agents and forwarding agent, without which the industry could not operate. The business knowledge base is vested in these partner companies and organizations which operate confidentially given the complexity and specialty nature of operations managed by commodity traders. Brand awareness being absent, the companies must discern themselves through service quality and risk management skills critical to the sustainability in the commodity sector. It is not common for commodity companies to trade together due to the sensitively to sharing market price and customer information, which is where LCTA enters as an important channel for communication within the commodity sector. LCTA has established a common voice for its members that can be more clearly understood when representing the sector before local, regional and federal authorities.

So, is LCTA also involved in training?

Sure. A highly developed skill set is necessary to efficiently and safely move commodities through the supply chain, which is dependent on professionals more than plant and equipment. LCTA organizes a series of annual training modules or courses open to members staff to extend or tailor their operational knowledge. Moreover, LCTA offers a scholarship to at least one candidate enrolled in the University of Lucerne’s Advanced Studies for Commodities Professionals course (CAS), organized in collaboration with LCTA and the Zug Commodity Association. The investment in skills development and higher education focused on commodities is central to the importance that professionals play in the success of the commodities business.

How LCTA has evolved over the last 10 years?

As mentioned, LCTA formed in 2010 with 8 founding members. Today’s membership has increased to 55 spanning a wide business range including: energy, gains and metals trading; precious metals refining; insurance and banking; and shipping and materials handling.

There is a significant concentration of companies active in the commodity sector in both Geneva and Zug, represented by respectively by the Swiss Trading & Shipping Association (“STSA”) and the Zug Trade Association (“ZTA”). In 2015 STSA established itself as the umbrella association for the entire Swiss commodities sector, LCTA and ZTA joining as Institutional Members. This was an important development given the need to collectively confront matters at the Federal level, with STSA best positioned to address.

How important is the commodity trading for canton Ticino?

The private character of the commodities companies makes it difficult to fully assess the economic contribution made collectively by the business active in the sector. In Ticino, we estimate that there are approximately 120 companies active in the commodities with around 75 million Swiss francs in tax revenue and provide an important contribution to the Canton’s GDP. In the international context, Switzerland is the world’s biggest commodities trading hub. Its global market share is estimated at 35% for oil, 60% for metals and 50% for sugar and cereals respectively. Some of the world largest companies are commodity trading firms domiciled in Switzerland. The importance of the sector in the safe and efficient global movement of goods should not be understated.

After more than a decade of globalization that promoted open markets and reduced trade barriers, the current movement is marked by the challenge of protectionist actions and retrenchment to nationalist policies invoking tariffs and quotas that are complex for commodity traders to navigate. The role of the commodity trader remains essential for moving goods and managing all the risk involved, but the difficulty of managing today means fewer small companies can survive. It is less about trading and more about shipping and storage of goods, payment risk mitigation, and capacity to finance an extended supply chain. This makes LCTA and its affiliate associations more important as a place where information can be shared between members and skills developed to meet the challenges of a changing marketplace.

What is your wish at LCTA for its 10th anniversary?

This is LCTA’s 10th year anniversary, which unfortunately is marked by the most threatening public health scary of our lifetimes. While there is no doubt that we will survive the health crisis, it is likely that the “new normal” will reflect a change in behavior both personally and professionally. I am an optimist by nature and believe that the changed behavior will be for the better not worse. For LCTA I believe and hope that the association will be made stronger platform and provide a more forceful channel for information sharing among its members, as well as a stronger voice to educate the public on the importance of the sector in moving basic goods from the source of origin or production to the point of consumption.

https://www.lcta.ch/site/wp-content/uploads/2019/11/GCC-2019-11-13-084.jpg8531280lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-06-25 12:00:002020-12-03 17:15:3210th Anniversary Of Lcta

The Responsible Business Initiative: Headstart for the KKS Counter-Proposal in the Conciliation Committee

Following back and forth consultations between the two Chambers (Council of States and the National Council), and with differences still remaining between both of them following the three votes, a Conciliation Committee was formed on June 4. After a fast discussion (only 45 minutes), the Conciliation Committee voted for the KKS counter-proposal with 15 to 11 votes.

This decision taken by the Conciliation Committee was then submitted for a vote to the National Council on June 8 and on June 9 to the Council of States.

The National Council accepted the decision of the Conciliation Committee in favour of the KKS counter-proposal with 99 to 91 votes and 6 abstentions.

The Council of States voted in favour of the KKS counter-proposal with 28 to 14 votes and 2 abstentions.

Therefore, the popular vote will take place on November 29, 2020 and the campaign will start this summer. This vote will be preceded by the popular vote of September 27 on the free movement of people with the EU: “For moderate immigration (Limitation Initiative)”, which may jeopardize the bilateral path Switzerland has taken in its relation with the EU until this day. As a result, until September 27, all national and local trade associations will be dedicated to contest the Limitation initiative.

KKS counter-proposal

The content of the Conciliation Committee’s proposal is in line with international standards. Firstly, the non-financial reporting duty is in line with an EU-Directive and the standards have been adapted to the conditions in Switzerland. Secondly, an additional due diligence requirement specific to risks associated with child labour in the value chain and trading of conflict minerals was introduced. These requirements go further than the current international standard and only the Netherlands have already implemented a regulation with similar content. As far as liability is concerned, the Conciliation Committee’s proposal adheres to the existing and internationally recognized liability provisions and eliminates any newly proposed liability provision, ensuring legal certainty (no reversal of the burden of proof).

Responsible Business Initiative

The initiative calls for the creation of a new liability provision of parent companies (large companies and SMEs in high risk sectors, such as mining and commodity trading) for wrongful acts of a controlled company (subsidiaries and suppliers) abroad. The catalogue of rights includes all internationally recognized human rights and environmental standards. The concrete consequences of such a liability provision, which would be unique internationally, are very difficult to foresee in detail. The initiative would increase legal uncertainty and; as a result, it will also endanger jobs, not only in Switzerland but also abroad. If a subsidiary of a Swiss parent company violates human rights, victims can directly sue the parent company in Switzerland for damages. To this end, the injured parties must be able to prove in court the damage suffered, its unlawfulness and an adequate causal link. If they succeed in doing so, the Swiss parent company would still have the possibility to free itself from liability, if it can prove that it has exercised all due diligence to avoid this specific damage (reversal of the burden of proof). In addition, Swiss courts would have jurisdiction in the event of liability claims, regardless of the existence of effective remedies in another country with a closer connection to the facts and a recognized legal system.

Florence Schurch Secretary general of STSA, is at your disposal to answer your questions: +41 22 715 29 90 / florence.schurch@stsaswiss.ch

https://www.lcta.ch/site/wp-content/uploads/2016/09/nave_01aw.jpg6601500lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-06-15 12:00:002020-06-15 12:00:00STSA update on the Responsible Business Initiative

On March 25, the Federal Council adopted an emergency ordinance on granting of credits with joint and several federal guarantees. Bridging credit facilities representing a maximum of 10% of their annual turnover and no more than CHF 20 million. Credits of up to CHF 500,000 will be fully secured by the Confederation, and will be paid out quickly and with the minimum of bureaucracy. Zero interest will be charged. Credit application form: covid19.easygov.swiss

Bridging credits that exceed CHF 500,000 will be secured by the Confederation to 85% of their value; the lending bank will secure the remaining 15%. Each company can obtain a credit of this type for up to CHF 20 million, which means a more rigorous bank review will be required. The interest rate on these credits is currently 0.5% on the loan secured by the Confederation. Companies with a turnover of more than CHF 500 million are not covered by this programme.

Dear Members of LCTA,

we would like to inform you that in March/April we received several emails and phone calls from LCTA members complaining that the measures implemented by the Swiss Confederation discriminate against trading companies. On the one side, discrimination on the access criteria; on the other side, discrimination on the criteria to establish the amount to be assigned.

Access Criterion

In fact, the “emergency ordinance on granting credits with joint and several federal guarantees” adopted by the Federal Council is discriminating against small trading companies that are not big enough to face the crisis alone and that unfortunately are not small enough to be supported by Confederation. Matter-of-factly, companies with a turnover <500 M CHF has no right to be supported by Confederations for these specific credits/guarantees; as you know, we are talking about companies with big turnovers (>500 M CHF), very small margins and not more than 20-30 employees.

Loan Amount Criterion

Also criteria to establish the amount to be assigned to companies (Covid19 credit and Covid19 plus credit) have arisen some doubts regarding the treatment of trading companies. According to the Federal Ordinance (25.03.2020), in the case of trading companies the benchmark for granting a Covid19-loan is turnover, while according to the Swiss Banking Association point 22 of the “SBA Q&A” (as of 02.04.2020) the benchmark is gross margin*. Obviously, for a loan to a company with CHF 30 million in turnover, there is a big difference between 10% of turnover (or CHF 3 million) and the gross margin* (in optimistic cases around 2%, or CHF 0.6 million). In addition, there are general indications or obligations (“it is appropriate or mandatory”?).

It is also a question of consistency: if for trading companies the gross margin criterion is used instead of turnover, then the access criterion must also be based on the gross margin criterion and not on the turnover criterion. This is a double standard case.

Our association (STSA, LCTA and ZCA) wrote a letter to federal authorities as well as to the Swiss banking association in order do have an official reply. This is an important occasion to remember that not all trading companies are giants and that there is a relevant number of the operators that was and is still negatively affected by this Covid-crisis without having the same rights of other similar companies.

*For the “Commodity Trade Finance” sector, which turnover parameters should be taken into account? (New question published on March 31, 2020): Traders in principle have high turnover figures. The use of annual turnover as a benchmark could therefore result in disproportionate amounts of credit being granted. In order to comply with the actual purpose of the transitional credit programme, the gross margin / gross trade margin should therefore be used. The gross trade margin is also used to cover salary costs and fixed and variable expenses.

https://www.lcta.ch/site/wp-content/uploads/2020/07/ART-Covid-Loan-claudio-schwarz-purzlbaum-a_DfqkONlm8-unsplash.jpg10671600lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-06-08 12:00:002020-06-08 12:00:00COVID-19 loan / COVID-19 plus loan: Discrimination for commodity trading companies

Fabio Regazzi, Member of the National Council, is working to find a solution for companies as regards the annual radio-television fee. He submitted in 2019 the parliamentary initiative “Excluding SMEs from the media fee”. The initiative has been deposited at the National Council on 19 September 2019, then has been approved by the TTC (Transport and Telecommunications Committee) and now it is at the Council of States.

In summary, Fabio Regazzi requested to amend the law on radio and television so that only companies with 250 or more (full-time) workers are subject to the radio and television fee. Companies with less than 250 employees should be exempted. Apprentices are not counted as employees.

If the initiative will be approved by the Council of States, the amendment to the law would only have to be approved by parliament.

https://www.lcta.ch/site/wp-content/uploads/2020/07/ART-Serfafe-tv-4308538_1920.jpg12801920lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-06-04 12:00:202020-06-04 12:00:20Update on the annual radio-television fee by Serafe

Spreading contagion – coronavirus effects on the working world

The rapidly evolving threat around the COVID-19 virus has raised concerns among the business and investor community across the world. The global and interconnected nature of today’s business environment poses serious risk of disruption of global supply chains that can result in significant loss of revenue and adversely impact global economies.

Enterprise response

As the uncertainty around the evolving event persists, we are starting to see companies take measured approaches to safeguard employees and mitigate financial and operational exposure. Companies and governments around the world continue to closely monitor the situation.

While cyber risk is a relatively recent consideration in resilience planning, companies have long maintained various resilience plans for business continuity, disaster recovery, and crisis management. These plans, while effective for a range of business disruptions, may fall short during a global crisis such as coronavirus or other pandemic events. Moreover, companies typically have less incentive to invest in distinct pandemic management capabilities since pandemics are lower-probability events (the last major pandemic, H1N1 influenza or swine flu, occurred in 2009). And while firms likely refreshed resilience plans in response to the H1N1 pandemic, it is important to consider differences in today’s environment. Companies must think through the implications to their businesses and develop specific crisis management annexures around pandemic threats.

Importance of pandemic planning – why traditional resilience plans are not sufficient to address pandemic-related disruptions

The differences between business disruptions that are caused by natural, human-made, technology or operational failures and those caused by pandemic events persist due to the potential increased scale, severity and duration of pandemic events, necessitating the need for organizations to expand beyond traditional resilience planning strategies. Companies must incorporate pandemic planning considerations into existing resilience management activities to provide a comprehensive response and to provide continuity for their most critical products and services. Additionally, companies should consider establishing pandemic-specific policies and procedures, capabilities for employee communications, telecommuting and personal/family leave to minimize disruptions.

Key takeaways – how to plan and respond differently to pandemics versus traditional resilience planning

Apply a people-first mindset: The very first priority of an organization during a pandemic should be the safety and well-being of its workforce. Employees are unable to focus on work responsibilities when their well-being and that of their family are in peril. It is important for companies to be able to monitor the situation, provide a safe workplace and offer their employees the support that they need. Examples of employee support may include providing access to internal and external resources (e.g., World Health Organization, International SOS, Centers for Disease Control and Prevention), services (e.g., extended child/elder care, transport for late hours) and recognition for employees who take on work for other areas, communicating timely updates to raise awareness and establishing employee standard of care services where possible to provide support to sick personnel or those that are caring for sick household members. To enable timely two-way communication and employee tracking and to disseminate critical information, companies must validate that emergency notification systems are in place and tested on a routine basis. In addition, companies should deliver pandemic-related training to enhance employee preparedness and alleviate any concerns.

Plan for geographical segmentation of functions and activities: A pandemic can have severe consequences in impacted areas and geographies, making them inaccessible for an extended period of time. As a component of a business impact analysis, companies identify the chain of activities and functions, along with interdependencies (e.g., people, process, technology, data, facilities, third parties) and related impacts, to inform potential mitigation strategies. From a pandemic planning perspective, companies should pay closer attention to the geographical concentration of these critical activities and functions, and how to segment them for work transfer to alternate locations and sites. As prudent risk management and to the extent possible, companies should look to diversify supplier base, customers and third-party service providers across geographies to avoid single points of failure.

Invest in technology and infrastructure to support remote work and virtual collaboration capabilities: A pandemic requires employees to stay home to limit exposure and to prevent or slow down the spread of the disease, requiring the activation of remote working capabilities. A pandemic may lead to a complete shutdown of the entire facility in an area, forcing a high number of employees to work remotely for an extended duration. This may in turn result in heavier-than-normal traffic on remote connectivity networks, causing capacity and load access issues. Companies should invest in tools to enable personnel to work remotely and collaborate virtually, perform periodic network stress testing and identify workarounds for critical tasks that are not executable from home. It is worth noting that remote working is a not viable option for manufacturing, thus resulting in critical impacts on product supply chains.

Consider the systemic nature of pandemics when designing response strategies: Companies must challenge and stretch the boundaries for traditional resilience plans to address pandemic events and carefully design distinct strategies; for instance, inter-affiliate contracts to subcontract work to or alternate supply chain vendors to overcome these barriers. Companies should validate that contracts between country-to-country affiliates are in place to reduce uncertainty of terms, rates, payments and regulatory requirements; data-sharing agreements are addressed within the contracts (e.g., General Data Protection Regulation requirements); and, as required in regulated industries, appropriate licenses are in place to conduct the additional work. Further, downstream dependencies should be considered. For example, if contractor onboarding is concentrated in the impacted region, capabilities in other locations that could be quickly mobilized should be entertained.

Assess reliance on third parties: Companies today have increased interconnectedness with third parties, which are also vulnerable to pandemic events. Companies must develop a thorough understanding of their critical third, fourth and fifth parties, and their resilience programs, and develop alternate plans, for instance insource strategies or substitutability, if the critical third party’s ability to perform services is impaired. Companies should also validate alignment between their alternate plans and those of their third parties. However, companies must recognize that their peers and competitors may look to the same third parties for assistance during a market contagion, leading to concentration risk. Where possible, companies must explore opportunities to embed contractual clauses that allow them to be prioritized for products and services in relation to their competitors.

Engage with customers: Customers are generally more empathetic to degradation or discontinuation of certain products and services during disruptions that are beyond a company’s control and involve life safety concerns than they are toward those that are perceived to be preventable (e.g., system glitches). However, they expect transparency and timely updates. Customers may have specific questions around a company’s supply chain, especially if resources are located in impacted areas, and also may have questions around how those resources may pose any potential risks to them for future use of the company’s products and services. A clearly drafted frequently-asked-questions document published and disseminated through multiple channels, including the company’s website and social media, can prove to be a useful tool to proactively address customer concerns.

Develop a robust communication strategy (including social media): Effective communications during any crisis are crucial to maintaining customer trust, restoring employee morale and confidence, and retaining market stability. For companies that have both retail and corporate customers, consistent messaging is key. All channels must reconcile (e.g., social media, customer call centers, public relations releases). Additionally, events like a pandemic can add another layer of complexity due to circulation of false news and narratives on social media. Companies must establish a robust communications strategy that clearly lays out process and protocols to engage with a wide set of stakeholders inclusive of any legal and jurisdictional considerations. For highly regulated industries such as financial services, health care, and power and utilities, companies should determine and comply with applicable federal, state and local reporting requirements (e.g., disclosure of material risks and impacts), and have a process in place to notify and engage with regulators proactively across various jurisdictions.

Team with public sector; national, state and local agencies; and health officials: Pandemics are a public issue first and a business issue second. Hence, it is important for the public and private sector to come together to provide an adequate and comprehensive response to a pandemic event. Companies must leverage advisories, resources and health safety measures prescribed by international, national and local agencies and health officials, and refrain from distributing conflicting materials as this can lead to confusion and fear among employees. Companies may set up matching-grant and other financial assistance programs to help employees and communities in financial distress during this time.

Increase rigor and complexity of testing: Companies must elevate the complexity of existing scenarios used for testing and simulations to assess preparedness for pandemic events. In addition, companies must rehearse crisis management governance and response, including C-suite executives and delegations of authority at least two levels down from primary decision-makers, so that delegates are well prepared to execute timely decisions in the event primary decision-makers are not available. Companies should also include critical third parties in select tabletop simulations to gain a better understanding of interdependencies and points of coordination, and to assess effectiveness of their resilience plans.

Leverage pandemic command center to prioritize and govern effectively: As time goes by, a widespread pandemic event will assert more pressure on existing resources, infrastructure and technology. As resources become constrained, firms must constantly re-prioritize delivery of products and services that are absolutely critical to meet customer needs and provide market stability. Equally important is a thorough understanding of activities that must be de-prioritized to allow effective repositioning of available resources. Companies must have a clearly documented prioritization framework, inclusive of associated risk tolerances, supported by a robust governance process to make risk acceptance decisions (e.g., discontinuation of certain services) during an event.

Establish crisis management exception approval process: In the event of a crisis, there are instances when companies need to deviate from standard policies and procedures to best meet the needs of their customers and employees. For instance, a company may not support or have stringent policies with regard to overtime or remote work, corporate card usage and so on during the normal course of the business; however, these policy exceptions may be necessary and permissible during an actual crisis. All potential changes to existing policies should be carefully reviewed by risk management, compliance and legal prior to being finalized and should take into account what risks are appropriate to accept.

What should companies do now?

Communicate with employees to raise awareness, enforce policies (e.g., travel restrictions) and familiarize them with available tools and resources

If pandemic planning considerations have not been incorporated into existing business continuity and disaster recovery strategies or updated, begin rapid planning or refresh of pandemic strategies and actions

Perform an immediate assessment of processes and functions with high manual intervention and critical third-party dependencies, especially in high-vulnerability and impact locations, to understand key risks, including any single points of failure

Review crisis communication plan and designate single points of contact to facilitate seamless engagement with local, national and global authorities, and other key internal and external stakeholders

Identify potential policy exceptions and institute a crisis management exception approval process to manage such exceptions on an accelerated basis in each jurisdiction

Confirm employees have the requisite capabilities, including access to requisite share drives, documents and other critical tools, to perform critical tasks remotely

Review relevant standard operating procedures and manuals and update them, as necessary

Monitor the situation and provide regular briefings to leaders on any emerging threats and issues

Ask employees to confirm and update contact information (primary and secondary) in company records, as necessary

Conduct brief pandemic training with employees to enhance employee and organizational preparedness to respond effectively

Contacts

Alessandro Cataldo, Ernst & Young Ltd, Lugano Partner, Transaction Advisory Services

https://www.lcta.ch/site/wp-content/uploads/2019/05/ART-Pandemic-Plan-diggity-marketing-s8HyIEe7lF0-unsplash.jpg10671600lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-05-08 12:00:002020-05-08 12:00:00Pandemic planning: Surviving through business as unusual

Over the last few years, there has been a significant increase in the level of connectivity that was hard to be expected.

Adopting IOT devices has become pervasive in the world of commodity trading. These detectors can be found almost everywhere in the chain of the commodity trading process, on ship containers, in the agriculture field in order to monitor land and production, in the oil field and inside mines. These technologies allow to monitor and predict anything that could slow down production and supplies.

Real-time trading. The central role of Internet of Things

The relation between Supply and Demand is the key of commodity trading. All goods must reach the right location at the right time. The Internet of Things allows to collect all real-time information which are needed to ensure that the whole process will not suffer of any kind of impediment. Do not forget all the online trading platforms where transactions take place at incredible rates.

What type of risks do these new technologies involve?

The described process has a very high level of technology, and it is sufficient to compromise a part of it in order to cause alterations on the market. Think about what impact a cyber-attack could have on the devices that provide all the information needed to manage Supply and Demand.

Why do IoT devices often have a low level of security?

One of the first issues is the use of default credentials in IOT devices, for example, the Mirai botnet took advantage of that to infect all the cameras. There are also market needs that encourage the lack of security in IoT devices. The high Demand forces manufacturers to produce new models, without paying the right attention to security issues and ignoring the current updates on older models, which have been replaced on the market by newer ones. Other than IoT devices, it is necessary to manage the whole communication system, which involves many actors in the commodity trading process, including producers, wholesalers, governments, regulatory agencies etc.

What repercussions could there be in the event of a cyber attack?

Definitely, one of them is the damage that could be caused by an actor who is able to alter the veracity of the information that is exchanged in the commodity trading process between the players mentioned before. In addition, there is the risk due to all those cyber-attacks that can reduce the availability of a player’s products by blocking its systems or damaging them, or even attacks that affect trading platforms. Think about the repercussions if a main supplier, such as an oil producer for example, were forced to stop the production due to a ransomware attack.

What is the correct approach that must be taken while facing this transformation?

The pervasive digitalization has brought many advantages, such as the introduction of the block chain technology which allows to not modify Bill of Lading and so on, or the ability to access real time data which used to seem impossible. As always, great possibilities also bring high risks, and that is why even the commodity trading world must approach cybersecurity systemically, considering every single element of the process connected to the Net and therefore, as a potential weak point. It is also necessary to work on security improvement in order to cope with the constant evolution of the cyber threat, protecting processes, technologies and especially training on this threats all people involved.

https://www.lcta.ch/site/wp-content/uploads/2020/02/internet-of-things_2.jpg16502625lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-03-03 12:00:002020-03-03 12:00:00Commodity Trading: the Internet of Things, new opportunities and new risks.

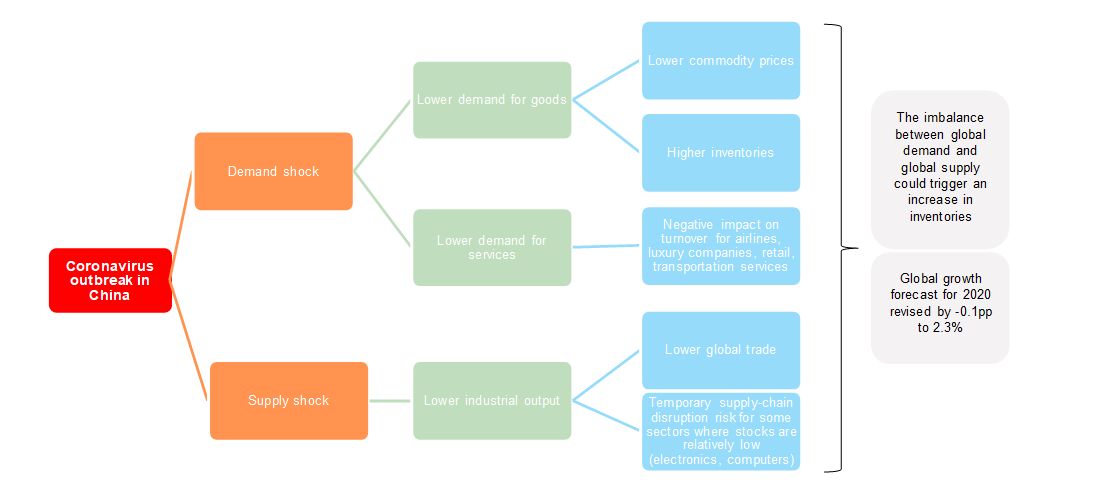

The hit to China’s GDP y/y growth caused by 2019-nCoV (Coronavirus) could amount to c. 1pp, mostly over Q1 2020. A recovery should thereafter be possible, based on pent-up production and policy support.

A protracted pause in Chinese activity could be disruptive for certain supply chains such as chemicals, transport equipment, textile and electronics.

If we look into the impact on the rest of the world: manufacturing and trade recessions are likely to continue, with a trade shock of USD26bn per week from the lockdowns in China and global growth barely staying afloat at +2% in Q1 2020.

First, the coronavirus outbreak is likely to keep the manufacturing sector in recession in H1 2020. Electronics and computers are most at risk. With the business interruption in China caused by the coronavirus epidemic, — which has put several sectors at risk of supply chain disruption and lower global demand — above long-term average stocks could increase further in sectors such as textiles, machinery and transport equipment and commodities. Meanwhile, goods’ shortages are a risk in sectors with below long-term average stocks (electronics, computers). In 2019, companies’ unusually high levels of stocks pushed manufacturing production into recession, notably in the advanced economies. With the stock absorption over the past few months being only partial, the lower global demand and the higher uncertainty are likely to push inventories up in the coming months. Hence, we expect the global manufacturing sector to remain in (shallow) recession in H1 2020.

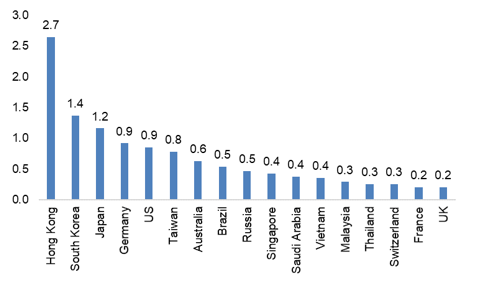

Second, potential losses of exports of goods and services to China could amount to USD26bn per week as production and trade are paused. We have revised down our global trade growth forecast for 2020 by -0.5pp to +1.3%. Hong Kong, the U.S., Japan, South Korea and Germany are most exposed. This weekly loss is more than the effect of the U.S.-China trade feud in 2019 (0.7pp). In terms of goods, the most exposed countries are Hong Kong, South Korea, Japan, Germany and the U.S. The cost could be USD18bn weekly.

Last, the macroeconomic impact should remain contained (-0.3pp on global GDP growth in Q1 2020 to +2%), if the business interruption in China doesn’t last for more than one month and business activity returns to normal after three months. While we think that the negative spillovers from the coronavirus epidemic will not last for more than three months, we doubt the global economy is strong enough to catch up entirely after the loss, given that the growth acceleration in H2 will be capped by U.S.-driven uncertainty. Overall, we think the recession in the manufacturing sector and global trade in goods will be prolonged into H1. Hence, we have revised our 2020 global GDP growth forecast by -0.1pp to +2.3%, based on a revised forecast for China (+5.6%, i.e. -0.3pp), the Eurozone (+0.9%, i.e. -0.1pp) and several other economies. We expect monetary policies to remain very active, with the ECB and the Fed even more likely to implement another rate cut in H1 2020, given that the “isolation” of China amid the coronavirus outbreak is likely to have strong negative impacts on both trade in goods and services.

Marco Arrighini Senior Sales Manager

Euler Hermes Switzerland | Via A. Adamini 10A | CH-6900 Lugano | Switzerland

https://www.lcta.ch/site/wp-content/uploads/2020/07/ART-Coronavirus-fusion-medical-animation-rnr8D3FNUNY-unsplash.jpg9001600lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2020-02-12 12:00:002020-02-12 12:00:00Coronavirus outbreak and the impact on global economy: USD26bn weekly in trade spillovers

On 25 June 2018, the EU Directive 2018/822 (DAC6), which introduced mandatory disclosure rules, entered into force. These rules target all kinds of cross-border arrangements that fall under a hallmark of the Directive, irrespective of whether an advisor or intermediary is involved or not.

When will the rules enter into force?

EU Member States have until 31 December 2019 to implement the new rules, which will be applicable from 1 July 2020. As of 1 July 2020, qualifying intermediaries (or, in certain cases, the respective taxpayer) will be required to disclose information on reportable cross-border tax arrangements to their authorities within 30 days of the earlier of when the arrangement is made available for implementation, ready for implementation or actually implemented.

However, intermediaries and respective taxpayers will also be required to disclose information retroactively by 31 August 2020 on reportable cross-border arrangements that have been implemented since 25 June 2018.

Which transactions will be affected by DAC6?

In order for a transaction to be reportable under DAC6, it is required that:

the arrangement has a cross-border dimension, i.e. it involves participants residing either in more than one EU member state or in a member state and a third country;

the arrangement falls under a hallmark; and

in the case of certain hallmarks, that the main benefit test is satisfied.

Who is required to report?

Under DAC6, the primary reporting obligation lies with the intermediary involved in the transaction.

In the following cases, however, the reporting obligation shifts to the taxpayer (individual or company):

The intermediary is exempt by virtue of legal professional privilege; or

there is no EU intermediary (in particular in the case of “in-house arrangements”).

Why DAC6 even affects ‘ordinary’ corporate groups?

As mentioned above, if a transaction falls under a hallmark, but there is no EU intermediary involved, the reporting obligations fall to the taxpayer residing in the EU, i.e., for example, to the EU subsidiary of a Swiss company.

The hallmarks that trigger a reporting obligation are drafted very broadly. They even catch standard transactions such as the following examples:

Example A: transferring functions to another country

A German group entity forming part of a Swiss based company transfers certain sales functions to its subsidiary in Poland, where taxes are lower. The additional income realized by the Polish company will be distributed to the German parent company, which leads to an overall lower tax burden.

This transaction may fall under hallmark B.2 of the Directive: An arrangement that has the effect of converting income into capital, gifts or other categories of revenue, which are taxed at a lower level or exempt from tax.

The main benefit test is satisfied if one of the main benefits of the transaction is a tax advantage, which is likely this case.

Therefore, this transaction must in principle be reported by the German subsidiary.

Example B: granting a loan to an Italian subsidiary

In December 2018, a Swiss holding company granted a loan to its Italian subsidiary. Whilst the interest is deductible in Italy, it is not taxable at cantonal and communal level in Switzerland (status of holding company). Even though the holding status will be abolished as of 1 January 2020, such transactions are caught by DAC6 because of its retroactive effect dating back to 25 June 2018.

This transaction may fall under hallmark C.1(d) of the Directive: An arrangement that involves deductible cross-border payments (…) where (…) the payment benefits from a preferential tax regime in the jurisdiction where the recipient is resident for tax purposes.

As one of the main benefits of this transaction is a tax advantage, the main benefit test is satisfied, too.

Therefore, this transaction must in principle be reported by the Spanish subsidiary.

Conclusion

Based on the above comments, DAC6 affects many Swiss companies with EU group entities. Non-compliance with these new rules is not an option, as some countries provide for penalties of up to several hundred thousand euros. Therefore, all Swiss companies with EU group entities should start analyzing their cross-border transactions now, so that they are in a position to comply with the reporting obligations as from July 2020.

Please find here the factsheet for additional examples.

Not sure if any transaction within your group might be caught by DAC6? Our specialist are available for a call or a meeting to explain you the potential impact of the Directive:

The Lugano Commodity Trading Association (LCTA) is pleased to offer a scholarship opportunity for the next CAS Commodity Professional (start: May 7, 2020).

IMPORTANT INFORMATION

Due to the COVID-19 emergency, the CAS Commodity Professional for the year 2020 has been cancelled.

Study content

Commodity trading and related services have grown significant in the Swiss economy, and they are expanding even further. These companies are in search of talents.

In cooperation with the Lucerne University of Applied Sciences and Arts, the Lugano Commodity Trading Association (LCTA) and the Zug Commodity Association (ZCA) offer a certificate of advanced studies CAS for commodity professionals. The certificate programme will provide attendants with a thorough understanding of the commodity industry and its characteristics. The course work will provide students from the commodity sector with detailed skills, students from commodity service providers the ability to better understand their clients, and give all graduates tools to enhance their careers. The CAS Commodity Professional combines theoretical know-how with hands-on learning experience provided by accomplished guest speakers. This programme prepares the participants to take on management or specialist functions within the commodity industry.

Basics of Commodity & Geopolitical Dynamics

Commodities within the value chain

Shipping and Transport

Trade Finance

Basics of Risk Management

Legal Aspects and Compliance

Scholarship amount: CHF 7,900 (CAS tuition fee)

Application requirements:

To apply to the LCTA scholarship, applicants must fulfil the following criteria:

Employee of a company, which is member of the LCTA

Tertiary education (as minimum level)

Good marks in the previous educations

Multi language. In particular, good knowledge of the English language (fully taught in English)

International skills

Letter of reference from the employer or from a key-person in the commodity trading sector

The scholarship is granted if the following conditions are fulfilled:

The student is required to have an 80% attendance at the lessons

The student has to pass all the exams

The student has to carry out a research on a topic related to the Lugano commodity trading hub (defined by the board of the LCTA)

IMPORTANT INFORMATION

Due to the COVID-19 emergency, the CAS Commodity Professional for the year 2020 has been cancelled.

https://www.lcta.ch/site/wp-content/uploads/2018/03/sld-scholarship.jpg4301500lcta_webmasterhttps://www.lcta.ch/site/wp-content/uploads/2024/05/LCTA-Logo-2024-r02-01.pnglcta_webmaster2019-12-02 12:00:132019-12-02 12:00:13Scholarship offered by the LCTA 2020

By clicking the "Accept" button, you consent to the use of all our cookies as well as those of our partners. We use cookies to collect information about your visits to our website, in order to provide you with an optimal experience and to continually improve the performance of our website. For more information, please read our privacy policy statement.

When you visit any website, it may store or retrieve information through your browser, usually in the form of cookies. Since we respect your right to privacy, you can choose not to permit data collection from certain types of services. However, not allowing these services may impact your experience.

These cookies are strictly necessary to provide you with the services available through our website and to use some of its features.

Because these cookies are strictly necessary for your enjoyment of the website, you cannot refuse them without affecting the operation of our website. You can block or delete them by changing your browser settings and enforce the blocking of all cookies on this website.

Google Analytics

These cookies collect information that is used either to help us understand how our website is being used or how effective our marketing campaigns are, or to help us personalize our website and application for you to improve your experience.

If you do not want us to track your visit to our site you can disable tracking in your browser here:

Google Fonts

We use Google fonts for typefaces on the site.

Video

We use cookies from YouTube and/or Vimeo for the integration of external videos on our site.